This essay tries to look at the Indian experience and pension reforms from the lens of accumalating longevity risks, and how it presents an opportunity for public and private sector reforms.

15 October, 2022

Mahesh Venkateswaran

What is common to Acko, Delhivery, Cadila Healthcare, SBI Life Insurance and Tata Realty?

They have a common investor in the Canadian Pension Plan Investment Board (CPPIB), a pension fund with over $500 billion in assets. CPPIB is one of over 20 state sponsored pension funds in Canada that are professionally managed, with substantial investments in public markets, infrastructure and other vehicles. According to an OECD report, the assets under retirement savings plan globally stood at $56 trillion at the end of 2020 with $35 trillion accumulated in pension funds. OECD countries totalled $54 trillion while the non-OECD countries accounted for the remaining $2 trillion. While the absolute contributions were quite significant in high income countries with pension assets equal to 100% or more of GDP, countries like India and China have relatively low pension assets (~20% of GDP).

India is an uneven social economy. On one hand, the GDP is rising to compete with global leaders, and on the other hand, being categorized as a lower middle income country, it is grappling with resources to fund its social protection systems and faces the middle income trap. Informalization of jobs and work contracts, which has been on the rise, also creates a poor asset base, which in turn pushes up social costs (like healthcare and income security) in the long term.

Pension reforms in India that commenced in early 2000s, for the first time, focused on the large informal workforce, and has seen mixed response. This is particularly relevant given over 80% of India’s workforce, of a total of 47.41 crores, is informal in nature and lack any form of pension or income security, thus making them extremely vulnerable to old age poverty. Government funded non-contributory social pension schemes and family support continue to the primary protection mehanisms against old age poverty for millions of older adults.

Mercers’ global pension index for 2022 evaluated 44 pension systems on three sub indices – adequacy, sustainability and integrity. With a score of 44.4 on 100, India was indexed as “D”, and scored the lowest in the IMETA (India, Middle East, Turkey, and Africa) region. The report made the following recommendations in improving the index score:

• Introducing a minimum level of support for the poorest aged individuals

• Increasing coverage of pension arrangements for the unorganized working class

• Introducing a minimum access age so it is clear that benefits are preserved for retirement purposes

• Improving the regulatory requirements for the private pension system

Pension system reforms in India

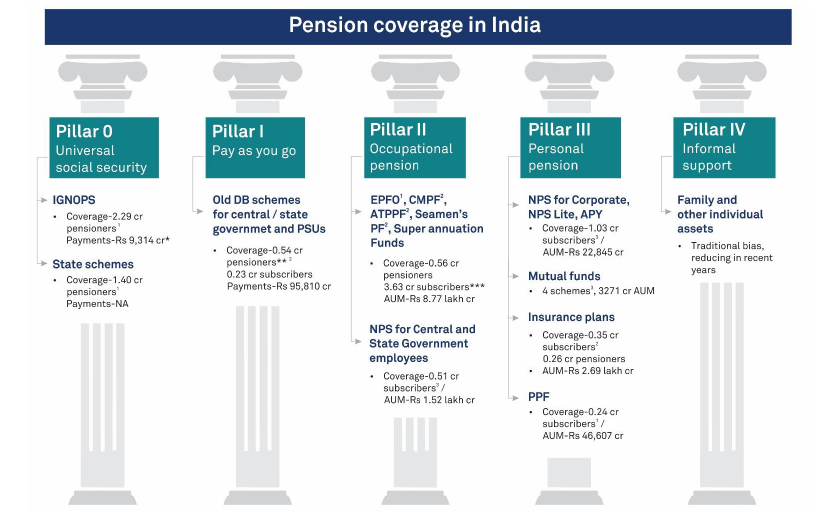

The Ministry of Social Justice & Empowerment, the nodal agency entrusted with care for older persons, in 2000, commissioned Project OASIS (Old Age Social and Income Security) to solicit recommendations towards building a shield against poverty in old age, for younger workers. Given the full cost towards pension benefits was borne by the Government, and led to higher burden year-on-year, the committee was also entrusted with the responsibility to devise new pension provisions that would ensure old age income security through modest contributions among younger workers. Subsequently, the Government established the Pension Fund Regulatory & Development Authority (PFRDA) and launched the new pension system (NPS), which was extended to informal sector workers in 2003. This marked the shift from a defined benefit (DB) to a defined contribution (DC) model, and led critics to point to evasion of its responsibility to ensure a social security net for the vulnerable populations. The contributory schemes continue to face the challenge of low awareness and education, and inadequecy and lack of sufficiency for its subscribers. This 2017 research study provides insights into how retirement products (like micro-pensions) can benefit the poor, and highlights the importance of financial literacy among other ways, to improve adoption. The NPS calculator illustrates the tentative Pension and Lump Sum amounts for various scenarios.

The Employees’ Provident Fund Organization (EPFO), a statutory body that predates the PFRDA, oversees three schemes – Employees’ Provident Fund Scheme, Employees’ Pension Scheme and Employees’ Deposit Linked Insurance Scheme – and continues to operate independently. The NPS and PFRDA systems provide a mix of mandatory and voluntary retirement and pension schemes for civil servants, public and private sector employees, and informal sector workers. The Atal Pension Yojana (APY), under PFRDA, for example, is a government-backed micro-pension scheme targeted at non-tax paying low-income informal sector workers, and has low associated charges. It is estimated that EPFO and NPS cover close to 47% and 8% of the organized sector while APY and NPS cover 3% of the unorganized sector. Despite the low contributions involved, the subscriber base of APY hasn’t increased substantially, and researchers point to uncertainty of long-term duration and less value realization adjusted to inflation as potential challenges.

Globally, pension systems design, reform and support has been a key policy intervention to mitigate old age poverty, and ensuring financial security for longer years of life. Started as defined benefit government plans for civil servants in the 1950s, India’s core pension schemes have shifted to a defined contribution model starting 2004, and the reforms initiated since (PFRDA, NPS, APY, etc) have largely toed this line.

The Asian Development Bank (ADB) was one of the sponsors of the research around the first phase of reforms, and since then, private sector participation in pension systems has increased substantially. The NPS registered pension funds are managed exclusively by the major banks and insurance companies (UTI, LIC, HDFC, Aditya Birla, Tata, ICICI, etc), and one can view updated fund level updates on the NPS site.

The World Bank’s five pillar pension framework provides a conceptual model to design, and determine the right approach to pension system reform based on primary criteria like adequacy, affordability, sustainability, equitability, predictability and robustness. PFRDA, along with CRISIL, came out with a report in 2017 to assess financial security of India’s elderly, and used the five pillar framework to evaluate India’s pension system and evaluate potential pathways.

The report broadly classifies states across India into two clusters, and recommends different (pension system) approaches given the general affordability among its populations. For example, it recommends promotion of market-linked products in cluster 1 and co-contribution model for cluster 2.

- Cluster 1 (Higher elderly population and higher per capita income (Aging cluster)

- Cluster 2 (Lower elderly population and lower per capita income (Young cluster)

Social protection and longevity risks

India is home to over 13.5 crore people over the age of 60 years and few have access to regularized income from savings, rental or pension. The governments (at the central and state levels), through a non-contributory social pension framework under the National Social Assistance Program (NSAP), provides basic income security for the old. Kerala, considered a model state when it comes to human development indicators (HDI) and home to a rapidly ageing population, relies to a large extent on modest contributions from various schemes and welfare board funds, and healthcare and local government networks, to provide financial and social security for its elderly. It is estimated that close to 50 lakh elderly are covered by one of five non-contributory pensions.

The figure below provides a glimpse of state contribution towards the Indira Gandhi National Old Age Pension Scheme (IGNOAPS), a non-contributory pension scheme for those living under the poverty line, outside the fixed contribution of Rs 200 per person (60-79 years) and Rs 500 per person (over 79 years) by the central government. Some of these contributions have been revised upwards over the last couple of years, yet overall quite low.

Since pension reforms were initiated in India, the demographic landscape, labour market, living and healthcare costs, family living arrangements and disease profile have changed significantly. With increasing life expectancy and decreasing mortality, people are also vulnerable to age-related ailments, susceptible to rising non-communicable diseases and disabilities (physical and intellectual). Together with unpredictability of market factors (inflation, drop in saving rates, health inflation, etc), those with modest savings or lack of income security beyond working years face grave financial longevity risks.

According to the latest Global Disease Burden report, non-communicable diseases like ischemic heart diseases, chronic obstructive pulmonary disease (COPD), stroke and diabetes are on the rise, and are major causes of death. Many of these conditions show high prevalence among the old, and thus pose a financial risk due to rising healthcare costs and health inflation. With low health insurance coverage across board, and particularly among older adults suffering with co-morbidities, it pushes up unplanned out-of-pocket expenditure, which comes from savings. This previous essay on longevity impacts delves into some of these aspects.

As per the Government’s LASI study, 45% of India’s health burden will be borne by the older population. Cost of caregiving (to support activities of daily living and specialized home care for elderly) is hardly accounted, and is another particularly contributing factor. According to this study, the annual household cost of caring for a person with dementia in India, depending on the severity of the disease, can range from INR 45,600 to INR 2,02,450 in urban areas and INR 20,300 to INR 66,025 in rural areas. While the assisted living sector is growing (and diversifying), it is beyond the reach of most, due to very high investment and monthly costs. Older women, particularly in a country with historically low participation rates in the workforce (< 30%) and lack of financial participation, are vulnerable in old age. Further, women also tend to live longer than men leading to feminisation of the elderly, and hence it is important to design pension policies exclusively for women.

Pensions funds and insurance-linked retirement plans that offer annuity products are usually designed by considering life expectancy and mortality projection models of their target population, and hence, susceptible to longevity risks, i.e., higher than expected payouts due to increased life expectancy. On the other hand, retirees and pensioners are likely to face market risk, longevity risk and inflation risk – all of which could lead to insufficiency of funds in later years.

A study by Agewell Foundation on the impact of Covid highlighted how many older workers are keen to re-enter the workforce, to gain financial independence for themselves and their families. With older informal sector workers not retiring, and putting themselves in precarious work environments, the burden on them continues unabated, and for many, social protection from the government is a lifeline more than anything. Participation in contributory pension schemes, in their current form, is still out of reach for millions.

In conclusion

Population ageing is a global mega-trend, and India with a mixed demographic profile, has an opportunity to effectively address longevity risks, a slow burning issue, through better planned public and private sector reforms. Given contributions and participation in such programs need to start early, pension funds and insurance providers have the opportunity to develop retirement and pension products that can ensure a high quality of life for those living longer in the future. The IMF has provided a detailed analysis on the financial impact of longevity risk, and warns of the rapid and potential deterioriation of public finances and private sector sustainability in cases where countries do not reform, to meet their demographic shifts. Piecemeal approaches to understanding longevity or forcefitting products (designed for a younger audience) for older population groups may be counterproductive. Ageing, and particularly longevity, is a multi-dimensional challenge, and it requires original and innovative solutions that are suited to the socioeconomic and demographic profile of the country.

Future of Ageing Newsletter

The Future of Ageing newsletter brings you news, stories and trends shaping the longevity economy in India and its impact on individuals, businesses, government and society. Businesses, brands, investors, startups, researchers, marketers and analysts following this space are likely to find it interesting.